Lifestyle

When Money Worries Make You Sick

Health Points

- Financial stress triggers the same physical responses as other chronic stressors, elevating cortisol and increasing risk for heart disease, diabetes, and immune dysfunction

- Money anxiety disrupts sleep quality, increases inflammation, and can accelerate cognitive decline in adults over 40

- Strategic financial planning that prioritizes health spending creates a psychological buffer that reduces stress-related illness

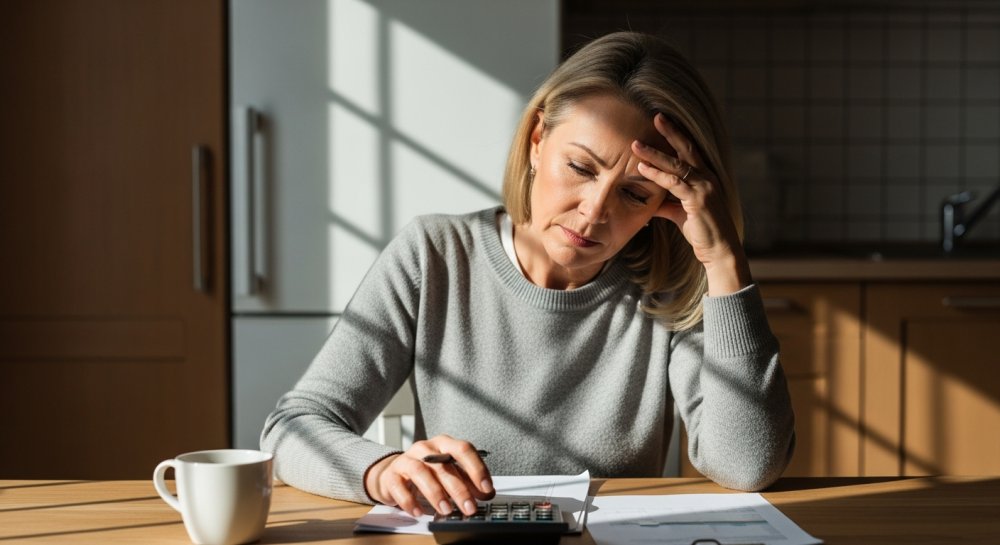

Financial stress ranks among the most consistently cited sources of anxiety across surveys and studies, and its effects extend well beyond bank account balances. For adults navigating their 40s, 50s, and beyond, the relationship between money worries and physical health becomes increasingly direct and measurable.

The body responds to financial pressure in the same way it reacts to any persistent threat. Cortisol levels rise, blood pressure climbs, and inflammatory markers increase throughout the system. These aren’t abstract reactions—they’re physiological changes that accumulate over time, contributing to conditions like cardiovascular disease, type 2 diabetes, and weakened immune function.

Research consistently shows that people experiencing financial strain report worse health outcomes across virtually every category tracked. They sleep fewer hours and experience poorer sleep quality. They’re more likely to skip preventive care appointments and delay filling prescriptions. The stress itself becomes a risk factor independent of income level.

What makes financial stress particularly insidious is its chronic nature. Unlike acute stressors that spike and resolve, money worries tend to persist, creating a sustained biological burden. For those in midlife and beyond, this sustained activation of stress pathways can accelerate cognitive decline and contribute to earlier onset of age-related conditions.

The connection works in both directions. Financial strain compromises health, and compromised health creates additional financial burden through medical costs and lost earning capacity. Breaking this cycle requires recognizing that health-supporting financial decisions aren’t luxuries—they’re fundamental infrastructure.

Prioritizing a financial cushion for healthcare needs creates psychological safety that translates into measurable stress reduction. Setting aside resources specifically for preventive care, quality food, and physical activity sends a signal to the nervous system that basic needs are secure. This sense of security has its own protective effect.

Financial control doesn’t necessarily mean having abundant resources. It means having a clear understanding of available resources and aligning spending decisions with health priorities. For many, this involves difficult trade-offs, but the framework remains consistent: financial planning should actively support rather than undermine wellbeing.

Practical approaches include automating contributions to health savings accounts, treating preventive care as a non-negotiable expense, and building modest emergency reserves before other discretionary spending. These steps create structure that reduces daily decision fatigue around health-related choices.

The psychology of financial control centers on agency. When people feel they have some influence over their financial situation—even within constraints—stress markers improve. Simple practices like reviewing spending patterns monthly, setting realistic health-related savings goals, and tracking progress provide this sense of agency.

For those over 40, the stakes of ignoring this connection increase. Chronic stress accelerates biological aging. Poor financial health that leads to poor physical health creates compounding disadvantages that become harder to reverse over time.

The goal isn’t eliminating all financial concern—that’s unrealistic for most people. The goal is preventing money worries from systematically undermining the health behaviors and medical care that become increasingly important with age. Financial planning that incorporates health as a core value rather than an afterthought provides the foundation for this approach.

Small structural changes often yield disproportionate psychological benefits. Designating specific funds for wellness spending, even modest amounts, creates mental separation between health needs and other financial pressures. This separation reduces the cognitive burden of constant trade-off decisions.

The evidence is clear: how you manage your financial life directly affects how well your body functions. Building financial systems that protect and prioritize health isn’t about wealth—it’s about recognizing that your most valuable asset requires ongoing investment and thoughtful stewardship.